Most financial institutions operate as black boxes. People are often asked to trust systems they don’t fully understand, with limited visibility into how their money is handled or how secure it is.

At River, we take a different approach, because you deserve to know your money is safe. Are your dollars and bitcoin ever at risk? Are you getting a fair price? What actually happens to your money?

In this post we want to help you understand how our business works so that you’re not left in the dark.

Table of contents:

Moving cash into your River account

For most clients, their first interaction with River is adding dollars to their account; whether to purchase bitcoin or grow their cash balance with Bitcoin Interest.

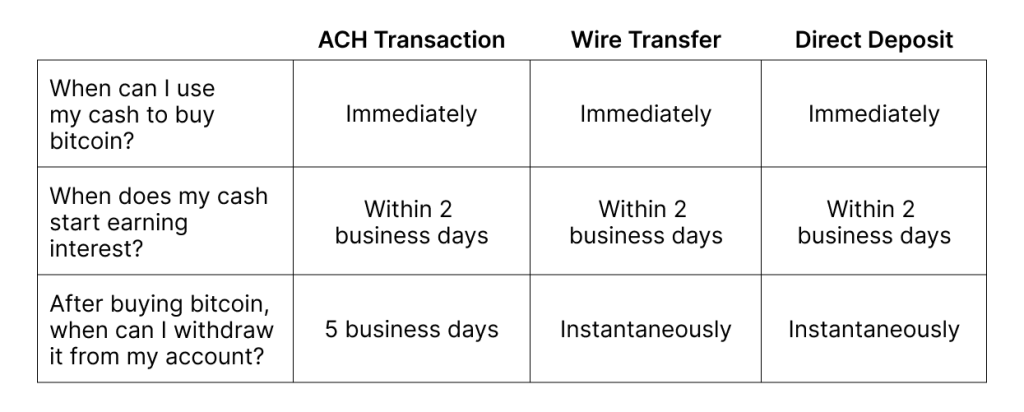

Clients can fund their accounts through a linked bank account (via ACH), a wire transfer, or direct deposit.

With a linked bank account, clients can purchase bitcoin immediately without needing to manually transfer funds. River enables this by advancing funds before the deposit fully settles.

Because River assumes risk when advancing funds, some withdrawal restrictions apply. The differences are summarized below:

Custody

Once funds arrive at River, the most important questions become: where does your money actually live, and how is it protected?

All client deposits, whether cash or bitcoin, are held exclusively on behalf of clients. River does not use deposits for lending, trading, or operational purposes. Security is the priority at every step.

US dollar custody

All client cash is held with our banking partner, Lead Bank, a federally chartered U.S. bank. River does not custody client cash on its own balance sheet.

This partnership is a deliberate choice that provides clients with several important benefits:

- FDIC insurance: Cash balances are insured up to $250,000 per depositor.

- Segregated accounts: Each client receives a unique account and routing number. Funds are not pooled.

- Bitcoin Interest on Cash: Lead Bank earns interest on deposits, and River passes those earnings to clients in cash or bitcoin.

Bitcoin custody

For client bitcoin deposits, we prioritize security above all else.

100% of client bitcoin deposits are held in cold storage. River’s custody system is built so that client bitcoin remains offline at all times, eliminating exposure to online attacks. To support day-to-day operations such as clients buying or selling goods and services, and withdrawals, River uses its own bitcoin in hot wallets, never client funds. Client bitcoin does not leave cold storage as a result of normal platform activity.

River’s cold storage infrastructure is built and operated in-house and does not rely on third parties. To reinforce transparency, River publishes a Proof of Reserves every month, allowing clients and the public to verify that River holds sufficient bitcoin to cover 100% of client deposits. This means clients do not have to trust River’s word, they can independently verify that their bitcoin is held in full reserve custody. While this may sound like a given, many popular exchanges still do not offer Proof of Reserves to their clients.

For readers who want a deeper technical breakdown of how River’s custody system is designed and audited, you can read our full report below.

Bitcoin transactions

When clients withdraw or send bitcoin from River, different systems are used depending on whether the transaction is made on-chain, over Lightning, or through River link.

On-chain and Lightning withdrawals

River maintains a hot wallet to process operational activity such as client bitcoin purchases and withdrawals. This hot wallet is funded exclusively with River’s own bitcoin, not client funds.

When a client initiates an on-chain withdrawal to move bitcoin to a personal wallet, the withdrawal is made from River’s operational hot wallet. This design allows clients to withdraw bitcoin at any time, without requiring client funds to be moved out of cold storage in response to individual withdrawal requests.

If a client chooses to withdraw via the Lightning Network rather than an on-chain transaction, client funds are first transferred to River’s internal Lightning account before being sent to their final destination.

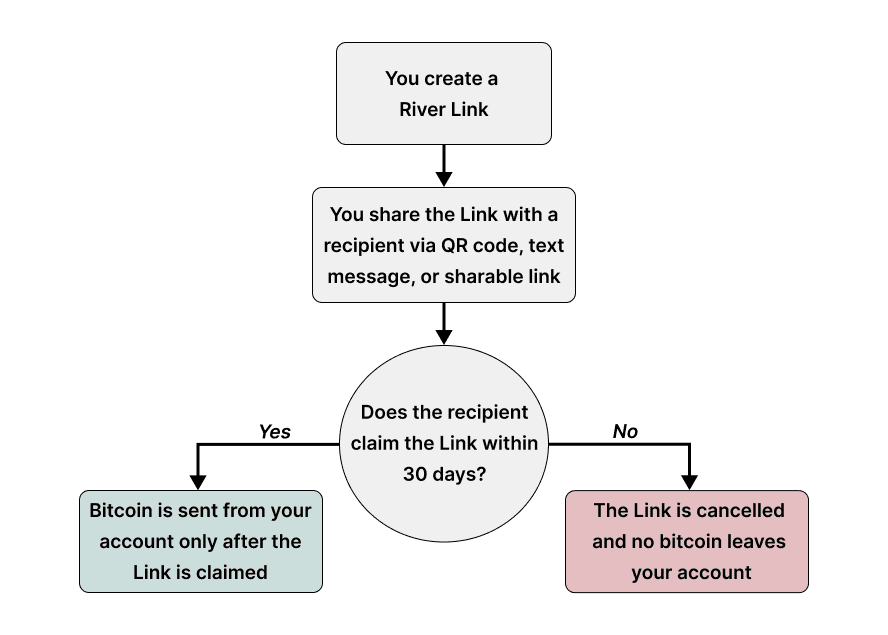

River Link

River clients can easily send bitcoin via text message or QR code with a River Link. Unlike typical bitcoin payments, funds are only moved from a client’s account once the recipient claims the link.

At that point, the payment is processed in the same way as a standard on-chain or Lightning withdrawal described above. If the recipient does not claim the link within 30 days, the Link is automatically cancelled without affecting a client’s bitcoin balance.

Withdrawal controls with ForceField

Some clients may choose to enable ForceField, which places restrictions on bitcoin withdrawals. ForceField is intended to reduce the risk of unauthorized withdrawals in the event of device loss, compromised credentials, or scams, while leaving other account activity unaffected.

When ForceField is active, clients can set a weekly limit on the amount of bitcoin that may be withdrawn and prevent new automatic withdrawals from being created or modified.

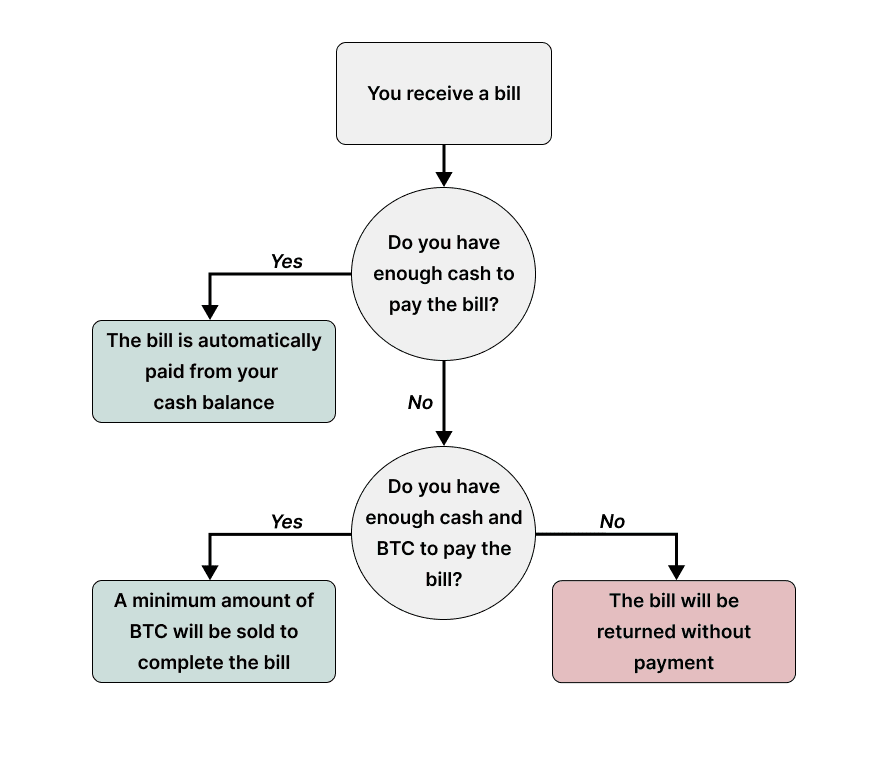

Paying bills

Clients can use their River account to pay bills like rent, credit cards, and utilities, or to move money from other financial platforms into or out of River. This is made possible by providing each client with their own unique account and routing number at Lead Bank.

When using your account for payments or transfers, you’re in control of how funds are sourced. You can spend from your cash balance only, or let payments pull from cash first and then bitcoin if needed.

The flow diagram below shows how payments are made if you choose to pay bills with both cash and bitcoin.

Bitcoin accumulation

River is a bitcoin brokerage, not an exchange. This distinction allows us to offer advantages that traditional exchange models cannot.

As a brokerage, clients buy bitcoin directly from River at a quoted price. This differs from an exchange, where the platform simply matches buyers and sellers in a marketplace. In that model, pricing and execution depend entirely on the available liquidity at that moment. At River, we take responsibility for both.

Getting clients the best price

Because River controls how orders are executed, we can focus on optimizing outcomes for clients. Rather than relying on a single exchange or counterparty, we source liquidity across a range of venues and evaluate pricing continuously in real time. This reduces the likelihood that clients receive stale or unfavorable prices, especially during periods of market volatility.

When a client places an order, they buy bitcoin from River. Separately, River manages its own positions by placing trades with multiple high-quality over-the-counter (OTC) desks that specialize in institutional-scale bitcoin trading. Our systems evaluate competing quotes and execute against the best available price.

Many platforms do not operate this way. During periods of market stress or rapid price movement, a single exchange or OTC desk can sometimes struggle to meet demand at fair prices, especially when a platform depends on only one or two liquidity providers.

As recently as October 2025, for example, some U.S.-based platforms sold bitcoin at prices up to $1,000 above prevailing market levels due to supply constraints. In these cases, elevated prices were not the result of intentional markups, but rather the automatic pass-through of unfavorable quotes from a limited liquidity source.

Risk management is a critical part of this process. River applies conservative limits to both the size and duration of open trades with each OTC desk. When we route an order, we commit dollars in exchange for bitcoin, and multiple client orders may be in flight prior to settlement. By enforcing strict exposure and time limits, River ensures it is never meaningfully exposed to market or counterparty risk, either in aggregate or with any single OTC desk.

Importantly, sourcing liquidity from multiple OTC desks is not about quantity, but quality. River continuously evaluates its OTC partners based on price competitiveness, execution reliability, trading capacity, and overall financial health, including balance-sheet strength. This ongoing assessment ensures we maintain relationships only with counterparties that consistently deliver fair pricing while minimizing risk.

These standards are mutual. Our OTC partners evaluate River with the same rigor, assessing our operational reliability and ability to settle trades as agreed. When that trust is established, they are willing to commit larger amounts of liquidity on our behalf. This, in turn, allows River to offer higher maximum buy and sell limits to clients without compromising on execution quality or risk management.

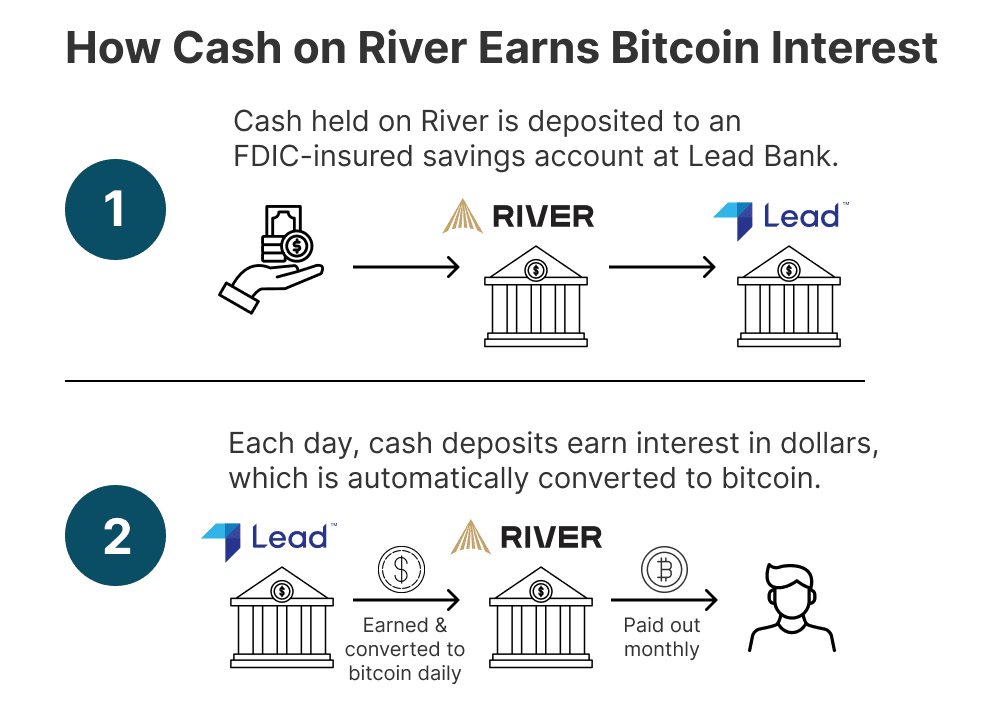

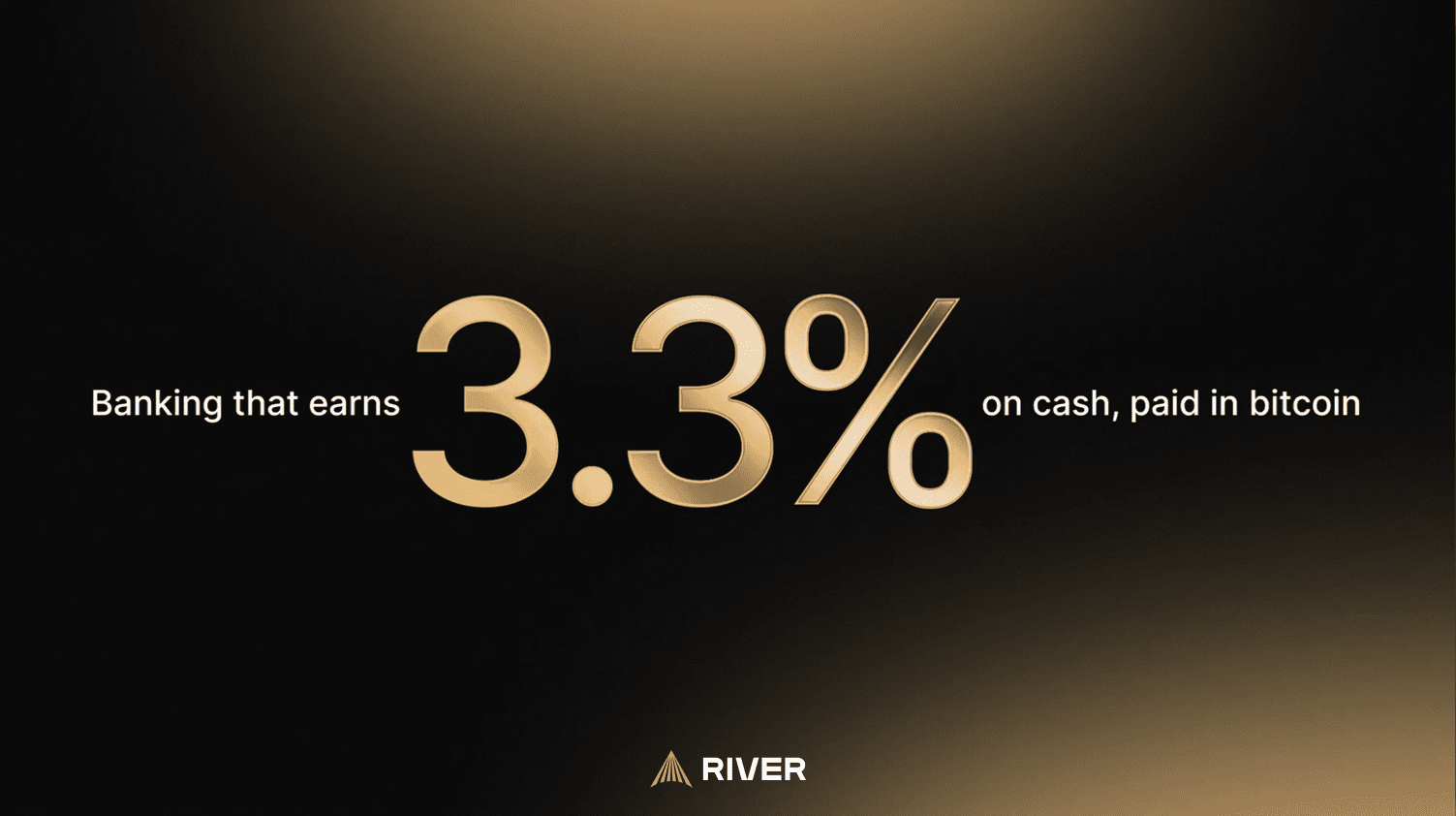

How dollars earn bitcoin interest

Cash deposits at all banks and financial institutions earn interest. However, most institutions keep a large chunk of these earnings for themselves, rather than giving it back to their clients.

At River, we believe that clients should keep as much of these earnings as possible. Since 2024, clients dollar deposits receive high rates of interest that are paid in bitcoin, and are FDIC-insured up to $250,000. This is made possible through our partnership with Lead Bank.

Client accounts accrue interest daily, which can be automatically converted into bitcoin. The bitcoin is paid out to clients at the beginning of the following month and can be withdrawn or sold immediately.

The interest rate that River can offer clients is ultimately tied to those set by the Federal Reserve. When the Federal Reserve cuts interest rates by 0.25%, it is common that River must also cut its interest rate by a similar amount. Likewise, when the Federal Reserve raises interest rates, River can offer a higher rate to clients.

Achieving frictionless money movement

River’s goal is to make your financial life easier in a world where people save in bitcoin and spend in dollars.

We build on Bitcoin as a foundation, with a focus on security and transparency. For clients who hold U.S. dollars, we offer competitive rates on FDIC-insured cash, along with tools to earn, save, and spend, all in one place.

Our approach is simple: prioritize security, keep costs low, and pass value back to clients wherever possible to help you build wealth.

You must be logged in to post a comment.